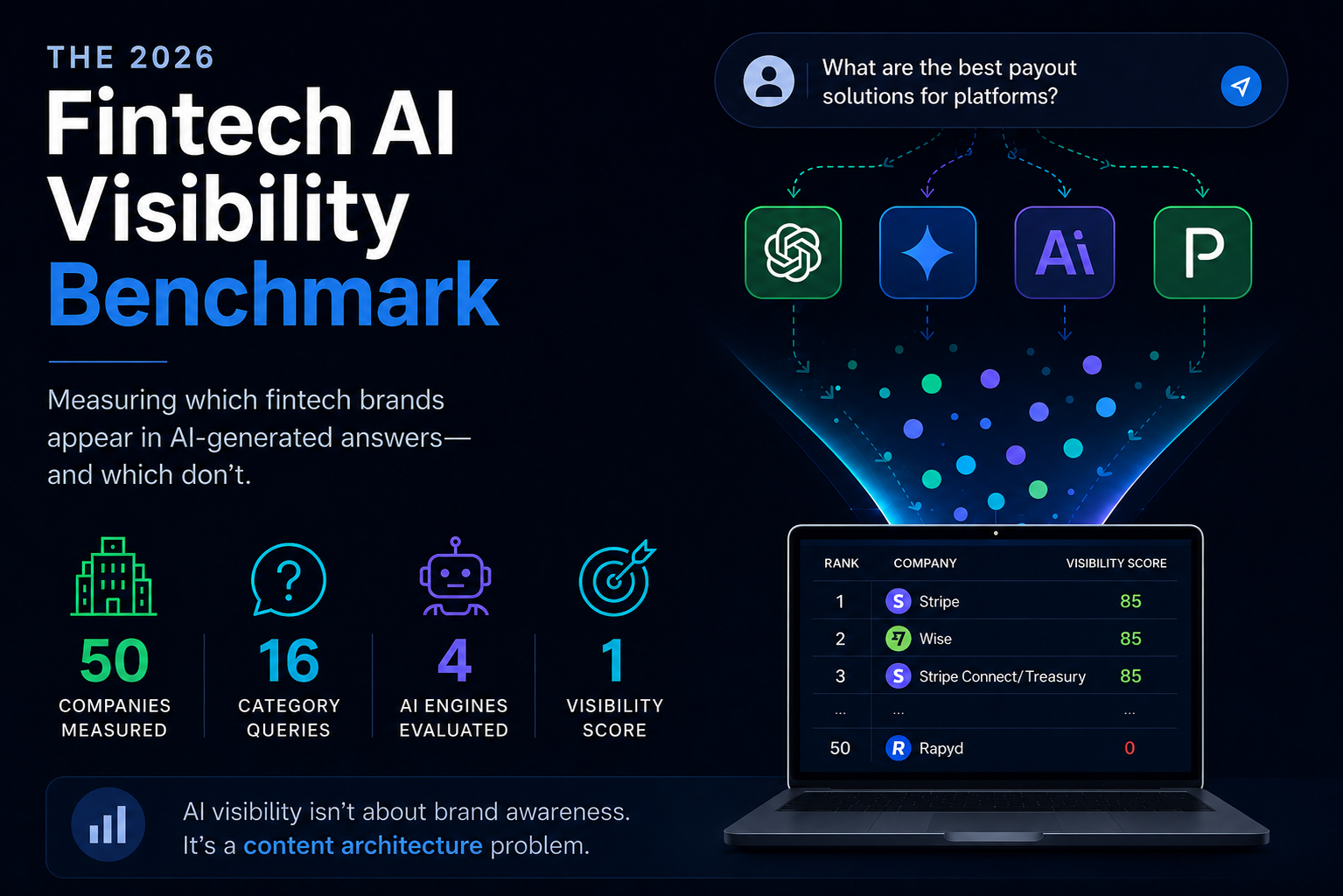

The 2026 Fintech AI Visibility Benchmark

16% of fintech companies are consistently visible in AI-generated shortlists. Here is who appears, who is absent, and what determines the difference.

Stripe (85), Wise (85), Stripe Connect/Treasury (85), Adyen (80), nCino (80), Kyriba (80), Unit (75), Mambu (75).

Rapyd, Remitly, WorldFirst, i2c, Sift, Featurespace, Provenir, and Peach Finance.

They appear in one engine but not in others, or in one query framing but not in another. Inconsistency, not invisibility, is the dominant condition in fintech AI visibility.

Same four engines. The buyer's phrasing changed the shortlist entirely. AI engines respond to specific category language, not just company names.

Every Highly Visible company appeared in at least 3 of 4 engines. No company with 2-engine coverage or fewer reached the Highly Visible status.

We measured 50 fintech and payments companies across ChatGPT, Gemini, Claude, and Perplexity on 16 unassisted category queries spanning eight fintech verticals. Data was collected on June 2, 2026.

8 companies (16%) are Highly Visible, consistently named across 3 to 4 engines. 8 companies (16%) are completely invisible. 28 companies (56%) exist in a gray zone: they appear sometimes, in some engines, for some query framings, but not consistently.

The strongest predictor of high scores was cross-engine coverage. Every Highly Visible company appeared in at least 3 of 4 engines. No company with 2-engine coverage or fewer reached the Highly Visible tier.

The most significant finding: query framing changed one company's score by 39 points. The same company scored 31 (Low Visibility) on generic BaaS queries and 70 (Partially Visible) on queries matched to its positioning. Same engines. Different outcome.

These results suggest that AI visibility in fintech is less about broad category awareness and more about association with specific buyer-intent queries.

+39 points. Same company. Same engines.

One embedded finance platform scored 31 when buyers used generic BaaS language and 70 when buyers used the platform's own category language. The AI shortlist changed entirely based on how the buyer phrased the search.

The 2026 Fintech AI Visibility Benchmark

When a VP of Payments evaluating payout infrastructure opens ChatGPT and asks for a shortlist, the answer she gets shapes the initial shortlist. Most of the companies in that category do not appear in that answer. They are not necessarily failing at brand awareness. In many cases, they are not being surfaced by the content, entity, and citation signals AI engines use to build recommendations.

We measured 50 fintech and payments companies across four AI engines and 16 unbranded category queries spanning eight fintech verticals: embedded finance, payments processing, payouts, cross-border payments, banking infrastructure, risk and compliance, credit and loan origination, and treasury management.

The core finding is that most fintech companies do not have an AI invisibility problem. They appear sometimes. The problem is appearing consistently. Answer engine optimization (AEO) and generative engine optimization (GEO) are emerging disciplines designed to improve visibility in AI-generated answers.

Why This Benchmark Exists

The buyer research shift is documented. G2 found that 51% of B2B software buyers now start their research with AI chatbots. Forrester's 2026 Buyers' Journey Survey found that twice as many buyers cite generative AI as their most meaningful research source as any other. These are not projections. They are current behavior patterns among the buyers fintech companies are trying to reach.

The problem is that the metrics most fintech marketing teams track do not capture this layer. Google rankings track traditional search. Domain Rating tracks backlink authority. Neither predicts whether a company appears in the AI-generated answer that forms a buyer's initial shortlist.

Ahrefs measured this directly. In a study of 15,000 prompts across ChatGPT, Gemini, Copilot, and Perplexity, only 11.9% of URLs cited by AI assistants ranked in Google's top 10 for the same query. More than 80% of AI citations came from pages that did not rank anywhere in Google's top 100.

That is not an SEO problem. It is a different problem entirely.

Two structural issues make fintech harder than adjacent categories.

The first is technical. AI crawlers parse raw server-side HTML. For some fintech sites, crawlability may be a prerequisite for earning citations because content rendered client-side may not be visible to AI crawlers. Product features in tab panels, pricing in interactive calculators, competitor comparisons in dynamic tools. These may not be accessible to the retrieval layer, regardless of how well written they are.

The second is YMYL. Fintech is a Your Money or Your Life category. AI engines apply more conservative source selection here than in general SaaS. The bar for earning citations is higher, the authority hierarchy (regulators, then established financial media, then fintechs) is more pronounced, and the timeline for building citation authority is longer. RankScience's analysis of financial YMYL content puts that timeline at 18 to 24 months.

What this benchmark measures and what it does not.

A high Visibility Score means a company appears in AI-generated answers for its category queries. It does not mean the company's product is the best in its category. A low score does not mean the company is failing. It means the company appeared less frequently in AI-generated answers for the benchmark query set. The reasons require separate analysis.

Methodology

50 fintech and payments companies across eight verticals. Selected for significance within their vertical by funding, revenue, or market position; clarity of category fit (unambiguous product category enabling clean entity recognition); and a mix of incumbents and challengers within each segment. Consumer-facing personal finance products were excluded. This benchmark covers only B2B fintech and payments infrastructure.

2 queries per vertical x 8 verticals = 16 total queries. All queries are unassisted -- brand names not included in the prompt. Prompt template:

"List the leading [query text] solutions. For each, briefly explain why you would recommend it and what distinguishes it from competitors."

| Q# | Vertical | Query |

|---|---|---|

| 1 | Embedded Finance / BaaS | best embedded finance platform for building card programs |

| 2 | Embedded Finance / BaaS | best unified embedded finance platform |

| 3 | Payments Processing | best payment processor for SaaS companies |

| 4 | Payments Processing | best global payment processor for enterprise |

| 5 | Payout / Disbursement | best payout platform for direct selling companies |

| 6 | Payout / Disbursement | best global payout orchestration platform |

| 7 | Cross-Border Payments | best cross-border payments platform for businesses |

| 8 | Cross-Border Payments | best B2B international payment API |

| 9 | Banking Infrastructure | best cloud-native core banking platform |

| 10 | Banking Infrastructure | best banking-as-a-service infrastructure for neobanks |

| 11 | Risk / Fraud / AML | best AML compliance platform for fintech |

| 12 | Risk / Fraud / AML | best identity decisioning platform for digital banking |

| 13 | Credit / Loan Origination | best loan origination platform for banks |

| 14 | Credit / Loan Origination | best digital lending platform for SMB lenders |

| 15 | Treasury / Cash Management | best treasury management system for midmarket companies |

| 16 | Treasury / Cash Management | best API-first cash management platform |

Engines: ChatGPT, Gemini, Claude, Perplexity. Private browsing mode, logged-out sessions, US-based IP. June 2, 2026. Responses captured manually and reviewed for company mentions using a standardized scoring rubric.

Formula: V = 0.40·A + 0.25·E + 0.20·D

| Component | Symbol | Weight | What it measures |

|---|---|---|---|

| Appearance Rate | A | 40% | % of a vertical's 8 possible runs where the company was named |

| Engine Breadth | E | 25% | How many of the 4 engines cited the company in at least one query |

| Query Depth | D | 20% | D receives full credit once a company appears in at least one relevant benchmark query |

| Tier | Score Range | Meaning |

|---|---|---|

| Highly Visible | 75–100 | Consistently named across category queries in 3–4 engines |

| Partially Visible | 40–74 | Appears inconsistently, in one engine or one query framing |

| Low Visibility | 10–39 | Rarely named; mostly absent from category answers |

| Invisible | 0 | Absent from all queries, all engines |

Maximum score under 2026 methodology: approximately 85. The remaining 15% is reserved for Citation Strength and Position Score components planned for the 2027 benchmark.

This benchmark uses 2 queries per vertical. The 2027 benchmark will expand to 10 queries per vertical for broader buyer-intent coverage. Scores reflect a single-day collection window (June 2, 2026). AI engine responses are non-deterministic and change over time. This is a dated snapshot, not a permanent ranking. The benchmark will be updated annually.

Planned for the 2027 Benchmark

- Position Score -- where in the AI response a company is named (first vs. buried)

- Citation Authority -- quality weighting for citation sources (trade press vs. vendor blog)

- 10 queries per vertical -- broader buyer-intent coverage

- Multi-week collection window -- stability measurement across time

Disclosure: PayQuicker (Payout / Disbursement) is a current DIGI CONVO client. This benchmark applied identical methodology to PayQuicker as to all 50 companies. No score adjustments were made. Results are reported as measured.

Benchmark Coverage

The benchmark evaluated 50 fintech and payments companies across eight verticals. Stripe is measured in two distinct buyer contexts -- its embedded finance products (Stripe Connect/Treasury) and its payments processing platform (Stripe) -- scored separately because they compete in different buyer verticals.

Overall Visibility Findings

| Tier | Companies | % |

|---|---|---|

| Highly Visible (75–100) | 8 | 16% |

| Partially Visible (40–74) | 28 | 56% |

| Low Visibility (10–39) | 6 | 12% |

| Invisible (0) | 8 | 16% |

The finding is not that 16% are invisible. That number is lower than pre-run estimates and reflects the binary structure of AI shortlists: either a company is in the answer, or it is not. The more significant finding is that 56% of companies occupy a gray zone.

They appear sometimes. In some engines. For some query framings. But not consistently. For a buyer doing research across multiple AI engines before shortlisting vendors, a gray zone company might appear in their ChatGPT search and not in their Gemini search for the same category. They might get one mention and then disappear from the next session.

Inconsistency is the dominant condition in fintech AI visibility. Whether it can be improved depends on the content, entity, and citation signals available to AI systems.

Engine behavior: qualitative observations

ChatGPT and Perplexity showed different company preferences for the same queries in several verticals. Perplexity surfaced companies that ChatGPT missed in Payout / Disbursement. Perplexity cited PayQuicker's own website directly for the payout orchestration query, while ChatGPT did not name it. In a separate instance, ChatGPT and Perplexity produced nearly identical responses for the same query, both citing the same third-party source. Different engines can converge on the same answer when both are retrieving from the same content.

Gemini consistently skipped companies that other engines named in Banking Infrastructure queries. Its BaaS recommendations diverged significantly from Claude's, with Gemini favoring US-chartered bank infrastructure and Claude surfacing more European BaaS providers.

No single engine reliably covered the full competitive landscape of any vertical. Cross-engine coverage is not a nice-to-have. It is what separates the Highly Visible tier from everything below it. Every Highly Visible company appeared in at least three of four engines. No company with coverage in two engines or fewer reached the Highly Visible tier.

Domain authority and AI visibility

The benchmark does not track Domain Ratings. But several Highly Visible companies in this dataset are known to have DRs well below the Partially Visible companies in the same verticals. Mambu, with a DR in the 60s, reached Highly Visible (75) alongside Stripe (DR 93). Visibility and domain authority do not appear perfectly correlated in this dataset.

External research points in the same direction. Ahrefs' study of AI-cited URLs found that only 11.9% of pages cited by AI assistants ranked in Google's top 10 for the same query -- suggesting that whatever determines AI citation is partially independent of the signals that drive traditional search authority.

Vertical-by-Vertical Breakdown

Embedded Finance / BaaS

| Company | V Score | Tier |

|---|---|---|

| Stripe (Connect/Treasury) | 85 | Highly Visible |

| Unit | 75 | Highly Visible |

| Highnote | 70 | Partially Visible |

| Marqeta | 70 | Partially Visible |

| Lithic | 65 | Partially Visible |

| Synctera | 43 | Partially Visible |

| Treasury Prime | 31 | Low Visibility |

This vertical shows the most query-framing sensitivity in the benchmark. Card-program and unified-platform queries surfaced a different shortlist than generic BaaS queries. Stripe Connect/Treasury dominated regardless of framing. Companies with more specific positioning (card programs, unified finance stacks) appeared in the query frames that matched their category language and were absent in others.

Stripe Connect/Treasury is the only company in this vertical to score near the ceiling (85). Unit emerged as the strongest pure-BaaS platform in this benchmark. The gap between them and the rest of the vertical is wider than in any other category except Cross-Border Payments.

Payments Processing

| Company | V Score | Tier |

|---|---|---|

| Stripe | 85 | Highly Visible |

| Adyen | 80 | Highly Visible |

| Worldpay | 65 | Partially Visible |

| Checkout.com | 59 | Partially Visible |

| Braintree / PayPal | 59 | Partially Visible |

| Square / Block | 31 | Low Visibility |

| Nuvei | 31 | Low Visibility |

| Rapyd | 0 | Invisible |

The most mature category in the benchmark. Stripe (85) and Adyen (80) are the category benchmarks against which everything else is measured. The gap between Adyen and Worldpay (80 vs. 65) is notable given that both are global enterprise processors. The visibility gap cannot be explained by market scale alone.

Checkout.com and Braintree are Partially Visible despite significant market presence and funding. Square scored only one appearance (Claude Q4) despite being a publicly traded company with strong brand recognition. Consumer-focused positioning does not appear to translate to enterprise AI shortlists. Rapyd is completely absent across all eight runs.

Payout / Disbursement

| Company | V Score | Tier |

|---|---|---|

| PayQuicker** | 59 | Partially Visible |

| Tipalti | 54 | Partially Visible |

| Payoneer | 54 | Partially Visible |

| Hyperwallet | 54 | Partially Visible |

| Trolley | 31 | Low Visibility |

| Airwallex | 31 | Low Visibility |

Initial testing with generic "global contractor" queries returned contractor management platforms (Deel, Remote, Rippling). None of the six companies in this cohort appeared. Shifting to "direct selling" and "payout orchestration" framings moved the cohort into measurable range.

PayQuicker's 59 reflects partial visibility when queries match its actual buyer language. The payout vertical is underrepresented in AI training data compared with payments and banking, which may help explain why scores for this cohort are lower than vertical maturity would suggest.

Cross-Border Payments

| Company | V Score | Tier |

|---|---|---|

| Wise | 85 | Highly Visible |

| OFX | 43 | Partially Visible |

| Currencycloud | 43 | Partially Visible |

| Remitly | 0 | Invisible |

| WorldFirst | 0 | Invisible |

What surprised us

Remitly scored 0 despite strong consumer brand awareness and significant market scale. Consumer-facing brand recognition does not appear to translate into enterprise AI shortlists for this category.

The clearest winner-take-most dynamic in the benchmark. Wise scored 8/8 and was named by every engine for both queries. OFX and Currencycloud each scored 2/8, appearing in only one or two engine responses. Remitly and WorldFirst are completely absent despite significant brand recognition.

Wise has a substantial content footprint across comparison pages, pricing documentation, and earned coverage in both fintech press and general financial media. Whether that footprint explains the 8/8 score is a hypothesis this benchmark cannot confirm. But the combination of broad coverage types that Wise has built is consistent with what AI engines typically draw on.

Banking Infrastructure

| Company | V Score | Tier |

|---|---|---|

| Mambu | 75 | Highly Visible |

| Thought Machine | 65 | Partially Visible |

| 10x Banking | 65 | Partially Visible |

| Finxact | 65 | Partially Visible |

| Galileo | 54 | Partially Visible |

| Temenos | 54 | Partially Visible |

| i2c | 0 | Invisible |

What surprised us

Finxact appeared in every cloud-native core banking query response, but not in any BaaS queries. The boundary between those two buyer frames is more distinct in AI engines than in the market itself.

This vertical shows a clean buyer-intent split. The cloud-native core banking query (Q9) consistently surfaced Mambu, Thought Machine, 10x Banking, and Finxact. Finxact appeared in all four engines for Q9. The BaaS for neobanks query (Q10) surfaced Galileo and Mambu, a largely different shortlist. Companies positioned around the "core modernization" buyer frame were absent from the "neobank launch" buyer frame, and vice versa.

Temenos, despite being the most widely deployed core banking system globally, scored 3/8. Finxact, acquired by Fiserv in 2022, appeared in all four engines for the cloud-native core query but zero for the BaaS query. That boundary is one of the clearest framing effects in the benchmark.

Risk / Fraud / AML

| Company | V Score | Tier |

|---|---|---|

| Socure | 65 | Partially Visible |

| ComplyAdvantage | 65 | Partially Visible |

| Alloy | 59 | Partially Visible |

| Sardine | 48 | Partially Visible |

| Unit21 | 31 | Low Visibility |

| Sift | 0 | Invisible |

| Featurespace | 0 | Invisible |

What surprised us

Socure and ComplyAdvantage owned completely different query frames with no overlap. In a vertical where both companies are credible for both problems, the AI shortlists were entirely separate.

The most striking query-frame ownership pattern in the benchmark. ComplyAdvantage scored 4/4 for the AML compliance query and 0/4 for identity decisioning. Socure scored 4/4 for identity decisioning and 0/4 for AML. Neither company dominates the vertical overall. They each own one query frame completely.

This pattern illustrates a dynamic that is likely not unique to this vertical: AI engines may be associating companies with specific buyer language rather than with broader category membership.

Alloy, at 59, appeared in both query types but owned neither. Sift and Featurespace are absent across all eight runs. Both are established vendors with strong product reputations. Their absence is a visibility gap, not a product judgment.

Credit / Loan Origination

| Company | V Score | Tier |

|---|---|---|

| nCino | 80 | Highly Visible |

| Blend | 65 | Partially Visible |

| Finastra | 59 | Partially Visible |

| LoanPro | 54 | Partially Visible |

| Provenir | 0 | Invisible |

| Peach Finance | 0 | Invisible |

nCino is the dominant answer for loan origination and the only company in this vertical approaching Highly Visible. Blend and Finastra appear consistently in the 3 to 4 of 8 runs range. LoanPro surfaces when the query framing shifts to "digital lending for SMB lenders," and both Gemini and Claude name it. Provenir and Peach Finance are absent across both queries and all four engines. Both are known in the market. Their absence from AI-generated shortlists suggests a gap between product recognition and AI search presence.

Treasury / Cash Management

| Company | V Score | Tier |

|---|---|---|

| Kyriba | 80 | Highly Visible |

| Trovata | 70 | Partially Visible |

| Nomentia | 54 | Partially Visible |

| HighRadius | 43 | Partially Visible |

| Coupa Pay | 43 | Partially Visible |

Kyriba is the dominant answer for treasury management and the only company in this vertical reaching near-maximum visibility under the 2026 methodology. Trovata scored 70 and appeared most frequently in queries focused on modern treasury workflows. Nomentia is recognized in European-oriented sources but was entirely missed by ChatGPT in the API-first query.

HighRadius and Coupa Pay each appeared in only two runs. Their AI visibility does not reflect their market position in AR/AP and spend management, categories with significant revenue and customer bases that have not yet translated into AI citation presence.

Full Results Dataset

The complete score table, all 50 companies, V scores, tier assignments, appearance rates, and engine breadth, is published separately on the benchmark dataset page.

What High-Visibility Companies Have in Common

| Finding | Why it matters |

|---|---|

| Remitly scored 0 | Strong consumer brand; zero enterprise AI shortlist presence |

| Finxact dominated Q9, vanished from Q10 | The clearest single framing boundary in the dataset |

| ComplyAdvantage and Socure owned completely different queries | Specialist framing appears more powerful than broad coverage |

| One company moved 39 points on a query wording change | Query alignment may matter more than domain authority |

How to Interpret Your Score

Invisible (V = 0)

Low Visibility (V = 10-39)

Partially Visible (V = 40-74)

Highly Visible (V = 75+)

Search your five most commercially valuable category queries in ChatGPT, Gemini, Claude, and Perplexity. Note which sources appear. If your company is absent from all five, it may indicate a broader visibility issue that warrants investigation.

The benchmark identifies visibility outcomes. Diagnosing the causes requires a separate analysis.

An AI Visibility Diagnostic applies this test systematically across your full query set, identifies the specific page types missing from your architecture, and produces a prioritized roadmap before any content is written.

What Would Change Our Conclusions

The benchmark would likely produce different outcomes under these conditions:

- Brand-assisted queries included: Queries that name a company directly (e.g., "Stripe vs. Adyen") would inflate scores for well-known brands and understate the gap between incumbents and challengers.

- Consumer fintech included: Consumer-facing brands like Remitly operate in a different citation ecosystem. Their AI visibility in consumer contexts may differ substantially from their enterprise scores here.

- Multi-week collection window: AI engine responses change over time. A single-day snapshot captures one moment. A four-week rolling window would reveal which scores are stable vs. volatile.

- Citation authority weighted: Not all citations carry equal weight. A citation from American Banker counts differently than one from a vendor blog. The 2027 benchmark will add Citation Authority as a scored component.

- 10 queries per vertical: Two queries per vertical is a narrow sample. Edge cases in query framing may over- or under-represent individual companies.

This benchmark measures what happened on June 2, 2026. The conditions above would each shift specific outcomes. They do not invalidate the methodology. They define its scope.

Frequently Asked Questions

Fintech AI visibility refers to how frequently and how prominently a fintech or payments company is named in AI-generated answers to category-level queries on ChatGPT, Gemini, Claude, and Perplexity. A company with high AI visibility appears on shortlists when buyers ask for the best embedded finance platform or the best AML compliance tool. A company with low AI visibility does not appear in those answers regardless of its Google rankings, domain authority, or brand recognition.

The Visibility Score is a weighted composite of three components: Appearance Rate (40%), which measures the percentage of relevant category queries where the brand appears across all four engines; Engine Breadth (25%), which measures how many of the four engines cited the brand; and Query Depth (20%), which is set to 100 for all unassisted appearances since all queries in this benchmark excluded brand names from the prompt. Under the 2026 methodology, the maximum achievable score is approximately 85. A Citation Strength component will be added to the 2027 benchmark, raising the maximum score to 100.

The eight Highly Visible companies in the 2026 benchmark are Stripe (85), Wise (85), Stripe Connect/Treasury (85), Adyen (80), nCino (80), Kyriba (80), Unit (75), and Mambu (75). These companies share one measured characteristic: broad cross-engine visibility. Additional factors such as content structure, category positioning, and citation presence may contribute, but were not directly measured in this benchmark.

The benchmark identifies outcomes, not causes. The most common pattern observed in this dataset is query-frame mismatch: a company has content built around one buyer framing, but the benchmark queries used different language. A company can have strong domain authority, active content programs, and significant brand awareness and still be absent from AI-generated answers if its content does not match the specific phrases buyers use. A second possible factor is technical: content rendered by client-side JavaScript may not be accessible to AI crawlers regardless of content quality.

The benchmark data suggests domain authority is a weaker predictor of AI visibility than it is in traditional SEO. Highnote, a unified embedded finance platform with a DR well below the incumbent leaders in its vertical, scored 70 (Partially Visible) using queries matched to its documented positioning. The benchmark observed several smaller companies outperforming larger incumbents in AI visibility. The underlying reasons require separate analysis.

Annually. The 2026 benchmark reflects AI engine behavior as measured on June 2, 2026. The 2027 benchmark will expand to 10 queries per vertical, add Position Score and Citation Authority components, and use a multi-week collection window to account for response variance across time. If AI engine behavior shifts significantly before the next annual update, a methodology note will be published.

No. The benchmark measures visibility in AI-generated recommendations, not product quality, market share, revenue, customer satisfaction, or category leadership. A low score does not mean a company has an inferior product. It means the company appeared less frequently in the benchmark's query set and collection window.

Download the Dataset and Methodology

The full dataset (all 50 companies, scores, vertical assignments, collection date, methodology version, and scoring formula) is available for download at the benchmark dataset page.

Want to See Your Score?

The benchmark measures 50 companies. It does not measure yours.

An AI Visibility Diagnostic applies this same methodology to your specific query set, your vertical, your competitors. You get:

- Category visibility across ChatGPT, Gemini, Claude, and Perplexity

- Engine coverage breakdown

- Query-frame analysis (which buyer framings surface you, which do not)

- Citation source audit

- Prioritized roadmap before any content is written

We run the audit before our first call. You see the gap before you spend anything.